Ker-Ker-Ker-RONA

- 0 Comments

- March 16, 2020

- by Curtis Taylor

- Leave a comment

Ker-Ker-Ker-RONA

Fear of the coronavirus appears to be more contagious in investment markets than in the real world with the Australian share market having fallen 26% and the US share market 26% since 20 February (today is Friday 13 March). Clearly that rate of decline won’t continue otherwise the All Ordinaries will be down to zero sometime after Easter.

The short term outlook is most uncertain however the long term outlook is good. Ultimately there are only two outcomes to the coronavirus. Either it will pass like every other major epidemic in history including the Spanish flu and the Black Death or it won’t pass. In which case how we invest our money will cease to be relevant. So if we are long term investors with a long term investment strategy and stick to our strategy the longer term will be fine regardless of what happens in the shorter term. It continues to be that growth investments like shares and property are expected to provide higher average returns over time than defensive investments like term deposits once the good and bad periods are averaged out. It also continues to be that Australian shares have a higher (and increasing) income of about 4-6% including franking credits compared with 1-2% (and probably going lower after the Reserve Bank cut rates again last week) for term deposits. So we should be sticking to our asset allocation strategies i.e. the proportion of defensive and growth assets in our portfolios including our superannuation and earning a reasonable income while waiting for the recovery.

The alternative is to sell, lock in a loss, miss out on the recovery and earn 1% on our money over the longer term. Which doesn’t sound like a viable longer term strategy to me. It may also be that we will get the best buying opportunities for at least the last two to three years.

It is however making for a lot of noise and many negative headlines to cheer you up. In the meantime it should be business as usual. We have just had the February profit reporting season in which companies have reported their profit results to 31 December 2019. It can take a lot of effort to wade through profit and loss statements, statements of financial position, cash flow statements, calculations of future intrinsic valuations etc. in order to form an investment view of a company. Tedious stuff indeed.

Here is a tip for efficient company analysis. Rather than doing the above what you do is go to the management commentary that accompanies the profit result announcement. If the company says something like our results were x or are going to be y because of the impact of the coronavirus you know it’s a poor result. If however, we find that there is the word despite rather than the word because so the company is saying our results were x or are going to be y despite the impact of the coronavirus you know it’s a good result. This is a much more time-efficient form of investment analysis. Incidentally, if a company is blaming its results to 31 December 2019 on the coronavirus that is a real worry and the stock should be avoided like the plague.

The attached article (The View: The Way We Were) by John Abernethy from ClimeDirect puts what’s currently happening into context. This article was published by ClimeDirect and is included here with the kind permission of ClimeDirect. For more information on or a free trial of ClimeDirect go to www.climedirect.com.au.

So if after reading the article and considering the reasons why you invest you have the urge to panic and sell good quality shares I prescribe a bottle of red. And if you still then have the urge to sell have another bottle and continue the process until you no longer want to sell good quality shares.

This blog does not make any recommendations. For sound long term financial, superannuation (including self managed superannuation funds) and investment advice please contact me at curtis.taylor@lifestylefstas.com.au.

The View: The Way We Were

Analyst: John Abernethy, Director

THE VIEW:

Way back in October 2011, I penned the following piece in The View as world share markets entered bear market territory.

https://www.climedirect.com.au/reports/content/202002/further-you-look-better-it-gets

The crisis had commenced in August when the US lost its AAA credit rating (and has not recovered it since), world capital markets were in turmoil and we were seemingly heading into a “Greek default” induced calamity. Many commentators at that time were suggesting that investors sell out of the equity market with the GFC still clearly in people’s memories.

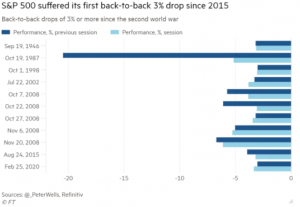

The parallels with today’s headlines in the mainstream press are clear to see. The current equity market correction, driven by the coronavirus, Covid-19, has given rise to the rerun of classic headlines like “Billions wiped off equity markets”, “Blood in the gutters” and the well-worn “Panic selling by investors”. The utilisation of the description “investors” rather than “speculators” gives the impression that rational people are frantically giving up their long-held investments and therefore you should too!

Source: Financial Times, Refinitiv

The disruption caused by the coronavirus is indeed concerning and not to be dismissed as an aberration. It will result in world economic data for (at least) the first quarter of 2020 being very weak.

Concerns that major events could soon be cancelled (think of the Olympics due to commence in Tokyo on July 24), that international tourists are calling off trips, that manufacturing supply lines are becoming frozen, etc, are all true and they paint a difficult short term outlook.

However, whilst I will not claim that there is never a good time to sell equities and re-allocate to other asset classes, I will categorically state that there is never a good time to panic and sell equities.

Equities (and never more so than today) offer exposure for investors to benefit from long term world growth emanating from the two major structural cycles at present.

The first cycle is haphazard and not as robust as it used to be, but does exist. It is the long growth cycle of the “developed world” as it drifts in and out of mild growth, slowed by ageing populations but benefiting from trade with the “developing world”.

The second concurrent and more powerful is the “developing world” growth cycle. In this cycle, which will endure for many more decades, hundreds of millions of people will steadily emerge from poverty into a better quality of life. This second cycle is propelled by urbanisation and technological developments, although it will periodically be checked by short-cycle downturns.

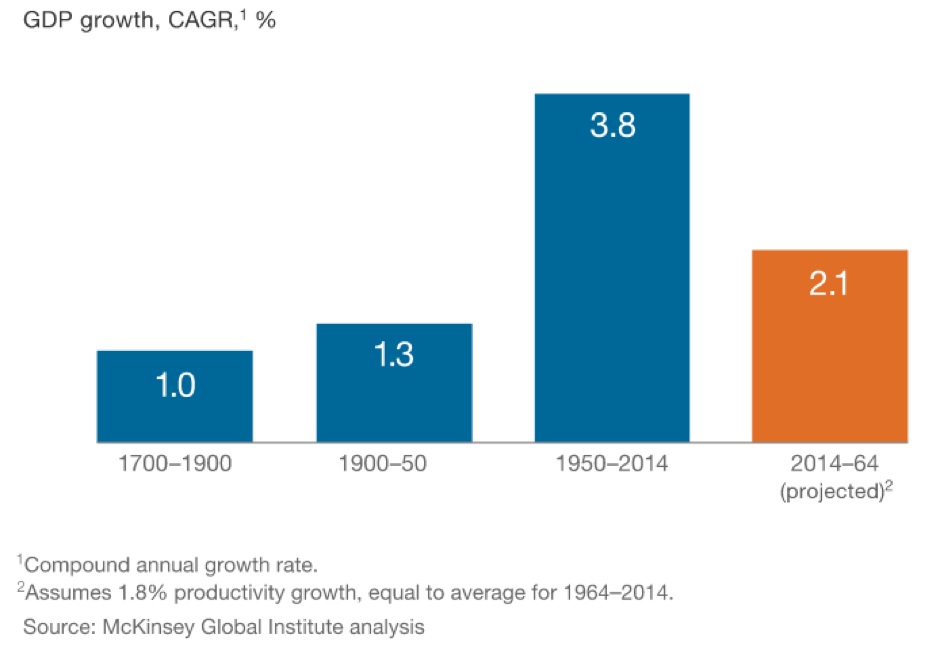

The developing world growth cycle will continue to drive the developed world cycle, so that total world growth continues to grow as it always has. Global growth will continue – albeit at a slower pace than experienced during the 64 years from 1950 to 2014, when it grew by 3.8% per annum.

The global economy is still growing, just not as fast as previously.

Clearly the coronavirus is a serious and developing problem for short term world growth as it will check both trade and the movement of people. However, it is very likely that it will be contained, managed and ultimately defeated, as has every other confronting virus in the past, including influenza, measles, Aids, SARS, MERS, Ebola, Zika virus and many others.

If the world does not defeat the virus, then all thought processes regarding investing for the future will become irrelevant. We should all go home and spend what time we have left with our loved ones.

Source: Financial Times

Some speculation of what may happen in coming weeks or months

As always, I believe the shorter term is harder to predict than the longer term, and more so when forecasting market movements and human behaviour.

However, observations of the past, particularly the last ten years, give us clues as to what the global central banks and governments will likely do if emotion and hysteria appear to be dominating markets.

Clearly the world’s major central banks will want to avoid a market meltdown that will in turn lead to economic recession. The central bankers have not spent ten long years printing money and manipulating interest rates that kept oxygen flowing to markets to suddenly give up and watch equity markets collapse

If central bankers have been prepared to buy government bonds, corporate debt, mortgage-backed securities and property securities (as in Japan), why would they decide that equities are a no-go zone?

Source: Financial Times

However, before central bankers intervene, they probably would regard the deflation of excessive valuations in some equity markets as desirable. A “healthy correction” may well be the collective view of central bankers, who should be equally concerned with the excesses and illogic of major bond markets.

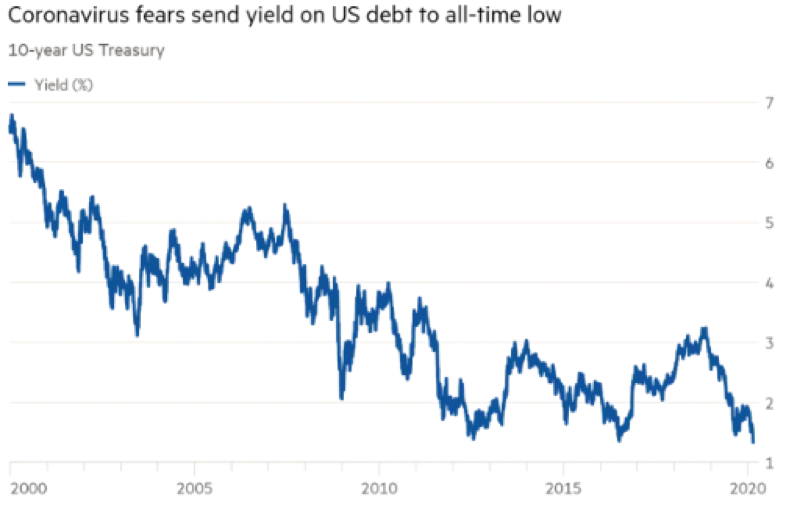

Whilst central bankers have caused the bond market bubble, they must surely be surprised (if not bemused) that some bond yields continue to drive deeper into negative yields. For instance, and remarkably this week, German thirty year bonds once again went into negative yield territory as coronavirus hysteria took hold.

In terms of the financial health of an investor, I wonder whether they are subjected to more financial risk from contracting the coronavirus or from being invested in a negative yielding bond for ten or twenty or thirty years?

Clearly as bond yields move lower, well below inflation and in some instances further into negative territory, the relative value of equities, given the long term growth trajectory of the world, becomes obvious.

Most important in periods of panic is the understanding that equities are perpetual investments. Good quality equities will return to growth after a setback. They did that after two world wars. They did that after an estimated 50 million people died in the Spanish Flu pandemic of 1918-19. They will recover and recommence to generate profit and cashflow. They will return to paying and growing dividends. Compare this to a negative yielding bond that is not perpetual and has a return profile that if held to maturity is negative!

Markets are driven by the sentiment of people buying and selling, and they (or we) are fickle much of the time. We become more desperate and terrified as prices fall, and happy through to ecstatic as prices rise.

The central bankers know this and will exploit this at some critical point in the future. They have proven for almost a decade that can convince even the smartest money or asset managers of the world that negative yielding bonds are a desirable investment for their clients.

Also, fiscal policy will swing into action and governments will use tax changes and monetary payments to stimulate consumers and businesses.

For instance, this week the Hong Kong government declared that all adult permanent residents in Hong Kong will receive HK$10,000 (A$1,950), and companies will receive a guarantee on loans taken out to pay wages and taxes – part of a HK$700m boost by the government to support the territory hit by coronavirus and political unrest. This is an example of “helicopter money” and it was previously used in Australia by the Rudd Government during the GFC.

Source: Zero Hedge

In Australia, we note that the Government has relented on its promise to produce a budget surplus in FY20. We predict that if the coronavirus continues to affect the Australian economy into the June quarter, substantial tax payment relief will be given to small and mid-sized businesses. This would help business cashflows at a time when stock levels are falling, or consumer sentiment is challenged.

There is much that can be done by sensible fiscal governance and there is little that the RBA through monetary policy can do other than ensure liquidity is plentiful in financial market and that banks do not restrict essential credit.

It will be an interesting few weeks and possibly months for markets. The coronavirus, the US election and the US China trade deal are amongst many other unknowns, but the likely behaviour or responses of central banks and governments is more predictable.

Is that a reason to be bullish in the short term? No. But it is a reason to remain calm, not panic and invest logically at a time when markets are being driven by wild speculation. The long term outlook for world growth looks good and that is what investors (not speculators) need to focus upon.

DISCLAIMER

Disclaimer: StocksInValue and associated websites are published by Stocks In Value Pty Ltd ACN 162 644 724 (Trading as Clime Direct), Authorised Representative of Clime Asset Management Pty Limited ACN 098 420 770 AFS Licence 221146. The information provided in this document is intended for general use only. The information presented does not take into account the investment objectives, financial situation and advisory needs of any particular person nor does the information provided constitute investment advice. Because of this, you should, before acting on any information on this website, consider whether it is appropriate to your objectives, financial situation and needs. Clime Direct does not guarantee the accuracy or timeliness of any information in this website, including information provided by third parties. We will not accept any liability for loss or damage as a result of reliance on the information including data, quotes, charts, opinions and ideas contained within this website.

Except for personal non-commercial use, you may not copy, publish, distribute or reproduce any of the information contained in this newsletter in any form without the prior written consent of SIV. If you have any queries please email Clime Direct at members@climedirect.com.au. Our full terms & conditions are available on our public website (www.climedirect.com.au/terms-conditions)

INVESTING REMINDER

Members, please note: investing in direct equity exposes you to the risk of capital loss. Before investing in any of these companies, we recommend you convince yourself, through your own research, that you agree with our theses or have an alternative positive thesis. It is also imperative that your portfolio weighting for any stock is consistent with your risk tolerance. Finally, we recommend you take a three to five-year view on all equity investments. These are not empty ‘caveats’, but the exact principles that our own fund manager partner makes, when investing on behalf of their clients – you should do similarly. Safe investing!

This note summarises the insights and understanding of Clime Direct at the time of publishing. Importantly, the understanding of our analysts will evolve in response to ongoing changes in company operating and financial performance, equity market conditions, internal research and discussions with management. As time passes after publication, reports become a less accurate reflection of the current thinking of Clime analysts. While analysts endeavour to publish frequently about stocks of interest to members, they are not able to comment on all company, market and internal research developments. For this reason members considering an investment based on our thesis are advised to always ensure they understand and still agree with that thesis, and are aware of the downside risks to their investment.

0 Comments